This is not investment advice. Always do your own research and speak to your adviser before making investment decisions.

Eighteen months ago, the case against investing in AI was a list of good questions. Is any of this real? If so, where is the revenue? When does the capex spending pay for itself? They were fair questions, and for a while the honest answer to each was: we will see.

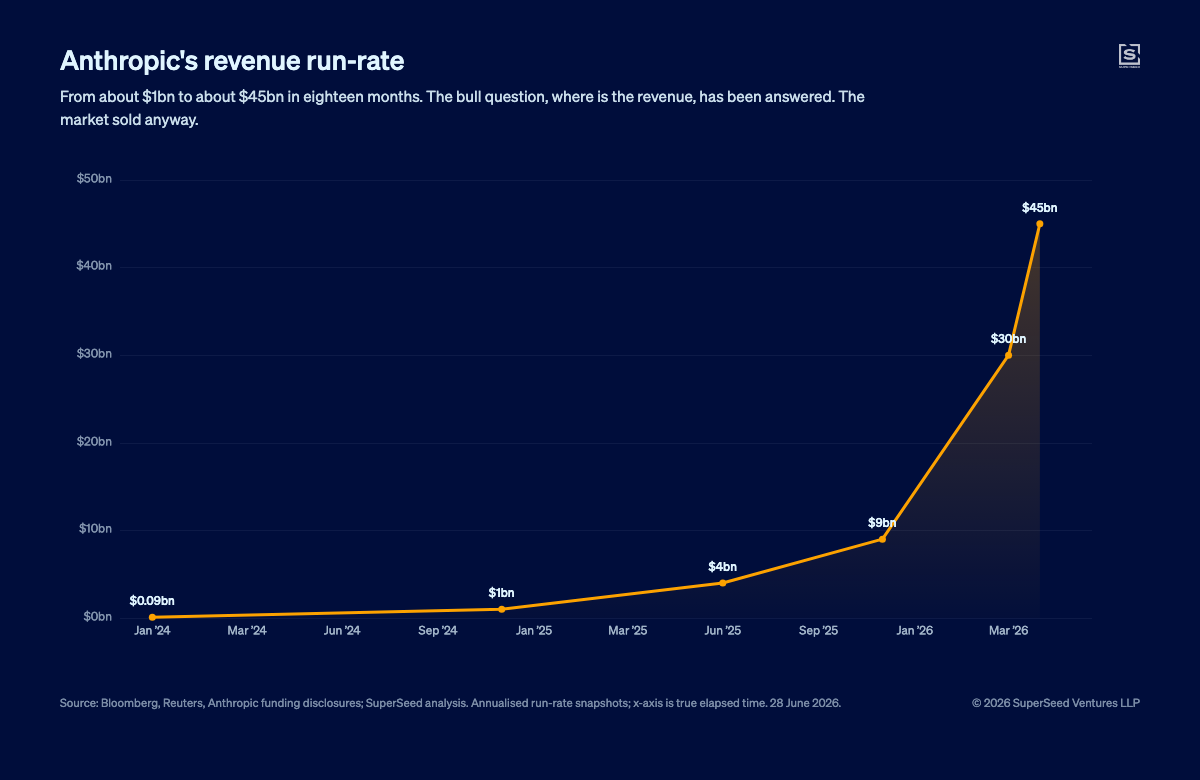

We have seen. This year the list was answered, line by line, in the bulls’ favour. The technology is real. We run almost all of SuperSeed on it now, and it has changed how we work more than anything in twenty-five years. The revenue arrived: Anthropic has gone from around $1bn to roughly $45bn of run-rate in eighteen months, the steepest revenue line in the history of software. The first hard returns showed up in the hyperscalers’ own numbers, where cloud margins widened as the AI backlog began to convert. And last week the most cyclical corner of the whole supply chain, memory, gave its proof: Micron printed the best quarter in its history.

The market took one look at the answered list and sold.

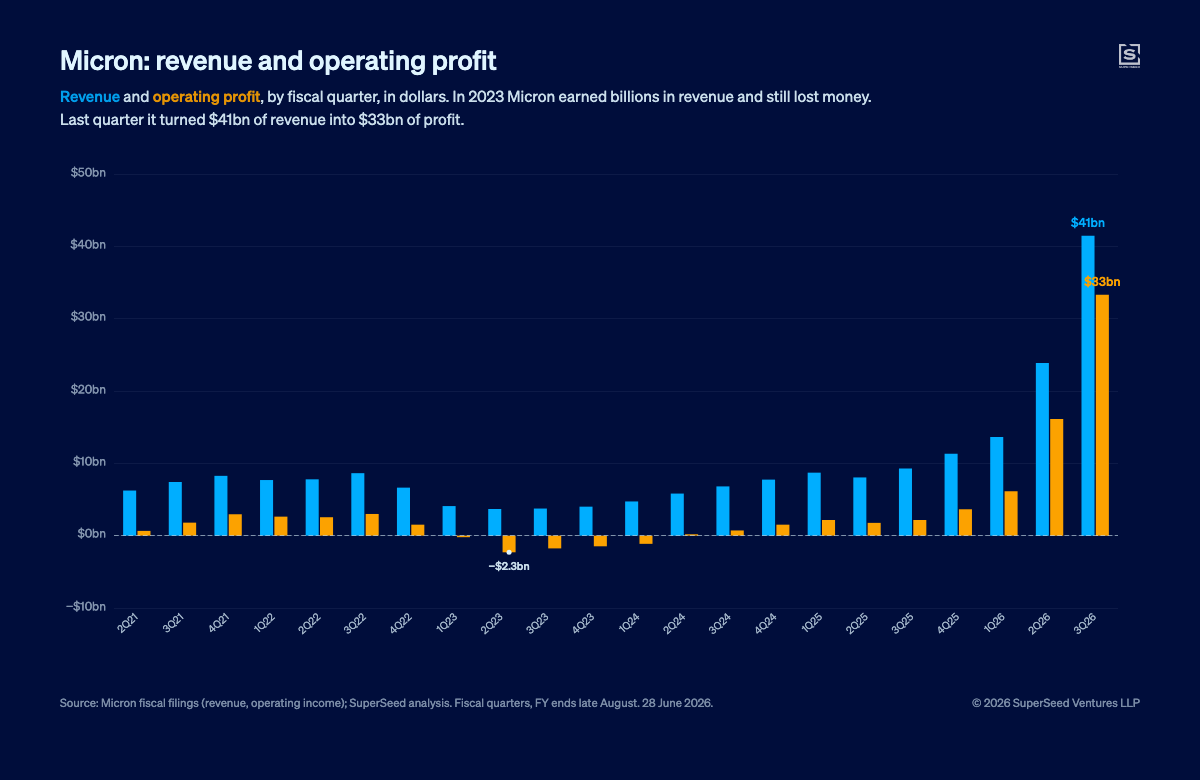

Micron’s result was far better than what had been expected. Revenue of around $41bn, more than four times a year earlier and comfortably ahead of forecasts. The fattest gross margin the company has ever reported, near 85%. An order book of roughly $100bn in contracted agreements stretching into 2027 and 2028, with guidance raised on top. By any measure a blowout. The stock had set an all-time high on the Monday, fallen around 13% on the Tuesday as the chip names sold off, reported its records after Wednesday’s close, jumped on the news, and then handed it all back. By Friday it was worth less than it had been on Monday. The best earnings in the company’s history could not sustain (let alone boost) the share price.

I don’t think that is noise. A share price is a claim on the future, not a receipt for the past. A boom is not most dangerous when its questions go unanswered. It is most dangerous when they have all been answered, and only one is left.

Answer “is it real,” and that question is closed for good. Answer “where is the revenue,” and that one closes too. Each answer is one fewer thing a bull can look forward to. Once the questions you can settle are settled, only the one you cannot is left: not whether the boom ends (since booms always do) but when.

I wrote last year about how the AI boom ends: negative margins all the way down the stack, and frontier labs that would have to become application companies or be commoditised. I stand by it. It is happening now. Which is why the question has moved on, from whether the boom is real to when it cools.

It comes down to the price of a thought

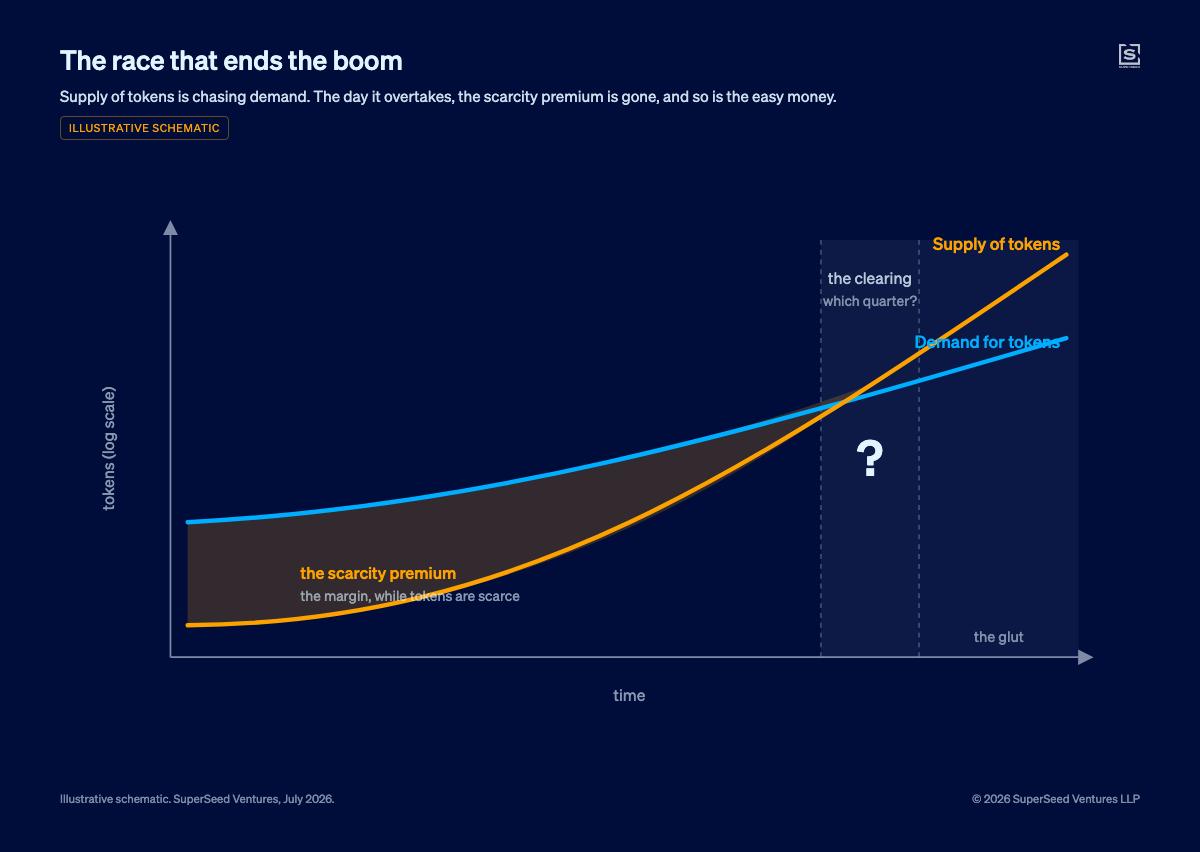

To see when, you have to be precise about what is actually being bought and sold. Not chips. Not data centres. Not even “AI.” The product of this entire industry is the token: one small unit of machine-generated thought. Everything upstream, the models, the GPUs, the memory, the power, exists to manufacture tokens. Nvidia sells the machinery. Micron sells a part of the machinery. The labs run the factory. The price the whole edifice rests on is the price of a token.

So “when does the boom cool” has an exact form. It cools when the cost of making a token falls faster than the world finds new uses for tokens. When supply outruns demand. That is all a glut is.

Both lines are moving rapidly, which is why it is so hard to call the timing. Demand for tokens is climbing exponentially. Every answered bull question is itself demand showing up. We use tokens at SuperSeed today for work we would not have dreamed of handing to software two years ago, and our own consumption has risen many times over even as the price per token has fallen.

But supply is also climbing rapidly, driven by two engines at once. The first is better models: each generation does the same work with fewer tokens, or better work with the same. The second is better hardware: each new generation of Nvidia silicon makes far more tokens per chip, and per watt, than the last. Combine those two curves and the supply of cheap intelligence compounds faster than either one alone.

Last year I followed a dollar up the stack. This year, follow a token down the curve. A unit of frontier-quality output that cost a certain amount in 2024 costs a small fraction of that today. A majority of the tokens now flowing through OpenRouter, the largest neutral marketplace for them, come from open-weight models, most of them Chinese, at a fraction of the Western price. One of the most-watched coding tools in the world, Cursor, turned out to be running a Chinese open model, Moonshot’s Kimi, underneath. The supply blade is dropping through the floor.

The bull answer to all this is “Jevons Paradox”: make a thing cheaper and people use so much more of it that total spending rises. That is true, and it is why revenue keeps climbing. But Jevons cuts both ways. While demand is being pulled up by cheaper and better tokens, supply is also being pushed up at a record rate. So demand can keep booming and we will still get to a place where we eventually overproduce: more tokens sold, less earned on each, far more capital spent to make them.

There is a serious case on the other side, and it deserves its strongest form. It says the glut never arrives, because demand for intelligence is unlike demand for railways or phones. You need only one phone, and you can sit on a train for only so many hours. But intelligence, once it runs on its own, manufactures its own demand, so the line may have no ceiling. On this view the constraint is supply: the handful of firms that hold the lithography, the packaging, the memory and the power. The old boom and bust in chips is over, the argument runs, so own the bottlenecks before the market stops mistaking them for cyclicals.

I find the first half genuinely persuasive. Demand for intelligence may be close to unbounded, and the supply chain really is a chokehold. But unbounded demand is not constant value, and that is the quiet substitution the argument makes. The first token that does something new is worth a fortune; the ten-thousandth that does the same thing is worth almost nothing. Demand can climb forever while the value of the next unit falls, and it is that second number that sets the price. So grant the infinite demand and the conclusion still holds: the boom cools not when we stop wanting intelligence, but when our ability to make the next token outruns the value of using it. The strong form of the other side, dressed up as the death of cyclicality, is in the end a claim that supply and demand no longer apply. If the facts showed that, I would change my mind, and the futurologist in me would be glad to. I do not think they show it yet. I am not ready to declare the laws of economics over.

Three ways it cools

So how does this resolve? Three ways, and they are not equally kind to the people who built the factory.

The Glut. Supply simply outruns demand. Models and chips keep improving on schedule, the price of a token keeps falling, and at some point it falls faster than even exponential demand can absorb. Tokens become almost too cheap to meter. Wonderful for anyone who uses intelligence, which is now everyone, and painful for anyone whose valuation assumed the scarcity was permanent. The squeeze lands first on the model makers, whose product is commoditising under them. That is exactly why Anthropic and OpenAI are racing into applications. The model is becoming a commodity; the product wrapped around it is where the margin survives.

The Wall. Before the glut arrives, supply hits a physical limit. Not chips, power. The binding constraint in 2026 is no longer the fab; it is the substation, the transformer with a multi-year lead time, the gigawatt data centre that has nowhere to plug in. Most of the capacity announced for this year is not yet under construction. This is the real case for putting data centres in orbit, and most of the bull argument for underwriting SpaceX: if there is not enough power on Earth, you go to where the sunlight is free and never sets. But even if space compute works, it does not save anyone from the eventual glut. It just builds a bigger factory and brings the glut forward, only a few years later than what would have happened on Earth. And here is the counterintuitive part, which matters most for the names that look safest. A wall does not rescue the chip and memory makers. A capped build means fewer chips bought, not scarcer chips sold at a permanent premium. A transformer shortage is not a Micron moat. It just moves the chokepoint from the silicon to the grid, and hands the rent to whoever owns the power.

The Jevons Surprise. Demand outruns supply anyway. Agents, robotics, whole categories of work we have not yet thought to automate, eat tokens faster than the factory can make them cheaper. The boom rolls on for years. This is the outcome I am personally most tempted by, because demand has surprised to the upside at every turn. But Jevons cuts both ways even here. A demand surprise keeps the revenue line climbing; it does not stop the cost of a token falling. The world gets vastly more intelligence, and the people manufacturing it keep less of the value in each unit they sell. The boom continues. The economics still narrow.

My bet

My bet? Certainly not a collapse in demand. I am about as bullish on what AI can do as it is possible to be, and nothing here is a bet against the technology. Anthropic’s revenue will keep climbing. So will the hyperscalers’. Micron’s next few quarters will probably be strong. So why did the best quarter in its history leave the stock lower?

Because a share price is a claim on the future, and the future the market has started to price is not this quarter. It is the one where the near-vertical growth of the last two years flattens into something ordinary. That quarter is possibly still years away. It does not matter. When you value a company like Micron, you are always pricing the slowdown you can see coming, not the boom you are living in. The market has simply started to price in the inevitability.

What I cannot give you is the date. We know how this ends: it ends when the cost of making a token declines faster than our appetite for more tokens. I lean towards that appetite surprising us for a while yet, because of how transformative AI is. But the market does not need the far side to arrive before it starts pricing it. It only needs to see it coming.

The bears had a list, and every question on it has been answered. That should have been the all-clear. Instead it was the starting gun, because a settled question stops holding a market up. Micron had the best week of its life, and the market looked straight through it to the other side.

None of this is AI failing. It is a market that has started wondering what AI is worth once the miracle becomes a utility. That quarter is probably still years away. But stock market prices never wait that long.