This is not investment advice. Always do your own research and consult with your IFA before investing.

Inflation and rates continue to set the agenda

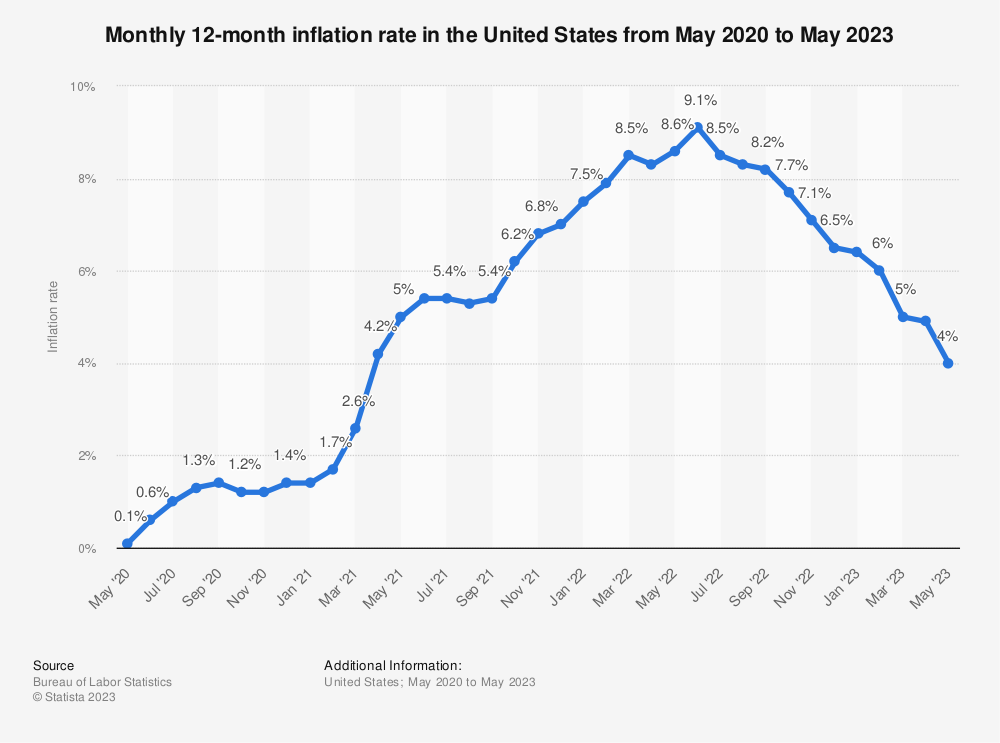

We have mostly had a warm summer here in the UK. It’s nice when it’s warm, but not good when things run too hot. This has been the case with inflation, with the year to May reported at 8.7%.

UK inflation numbers are in sharp contrast to their US counterparts. The Fed’s headline inflation rate was reported at 4% in May (down from a peak of 9.1% last summer). It is expected to decline further to 3.6% in June.

Over the past year, we’ve all intensely discussed the accuracy of the official inflation statistics. At times, it has felt like they were lagging behind what we experienced in the real economy. And it is true – the method for putting together inflation statistics in the US and the UK is still relatively old fashioned, prone to lag.

The team over at Truflation has put together an alternative inflation indicator. Their US numbers are even more upbeat, estimating current US inflation at 2.46% (with the UK still behind).

With inflation down, US rates rises are now on hold. Although Fed chair Jay Powell has cautioned that there might be more rates rises coming, it looks like the worst is over for now.

GDP Growth and corporate earnings – not a disaster

Whereas many had expected recession to hit the US economy in 2023, growth has held up (albeit modestly). US Q1 GDP growth was at 1.3%, and Q2 is forecasted at 1.1%. Not a celebration, but not recession either.

Corporate earnings held up reasonably in Q1. They are expected to decline in Q2 due to a combination of modest revenue decline and cost pressures. However, that decline was largely priced in at the start of the year. The analysts forecast that earnings growth will resume for the second half of the year, now that the worst of the inflation pressures are behind us.

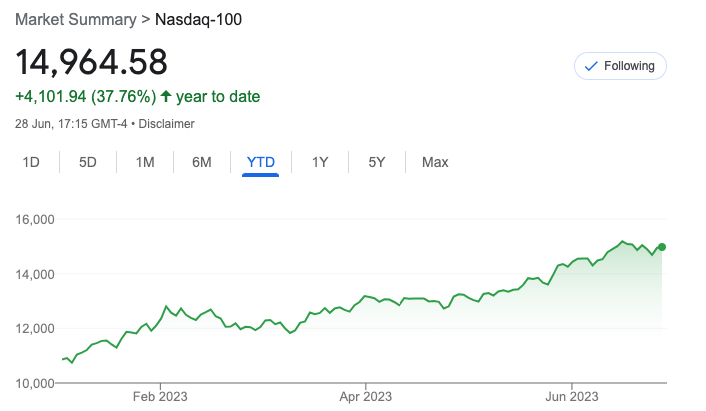

Could this just be the heralded soft landing? Some investors think so. The S&P500 has rallied ~15% this year, and the Nasdaq-100 35%. True, up to May, the rally was largely driven by the 7 mega stocks (Microsoft, Apple, Google, Meta, Amazon, Tesla and Nvidia). But over the past month, the gains have been more broad based. They now include almost all sectors outside oil&gas, FMCG and pharma.

Time to pile back into stocks?

So with inflation down. It is time to pile back in?

There are two main threats lurking:

- stocks still look quite expensive, and this year’s rally hasn’t helped. Forward P/E estimates on S&P500 are at 19.4x and the earnings yield is at 4.5%, which you can compare to the 12 months US treasury yield of 5.25%. The equity risk premium seems to have all but disappeared. Unless you compare to 10-year treasuries, which -see below:

- The US treasury yield curve is still deeply inverted. The 10-year spread is -2% (meaning you can get 2% more in interest on a 3-months bond than on a 10-year bond). This is something that historically has been a strong harbinger of recession.

And round and round it goes. Things look better than feared and stocks are up. But forward looking indicators are orange/red, and there might be a correction on the way. Expect more volatility ahead.

Private markets

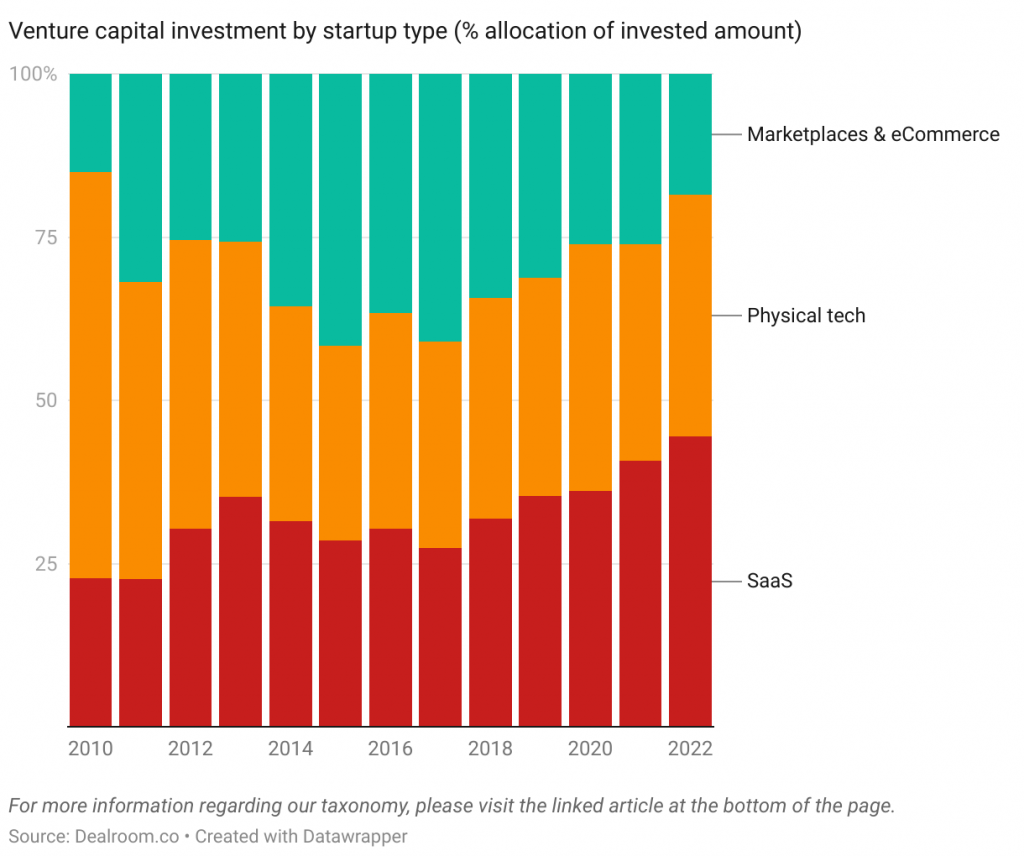

The venture capital ecosystem continues to bifurcate. Between growth/late stage and early stage. And between AI/SaaS and everything else.

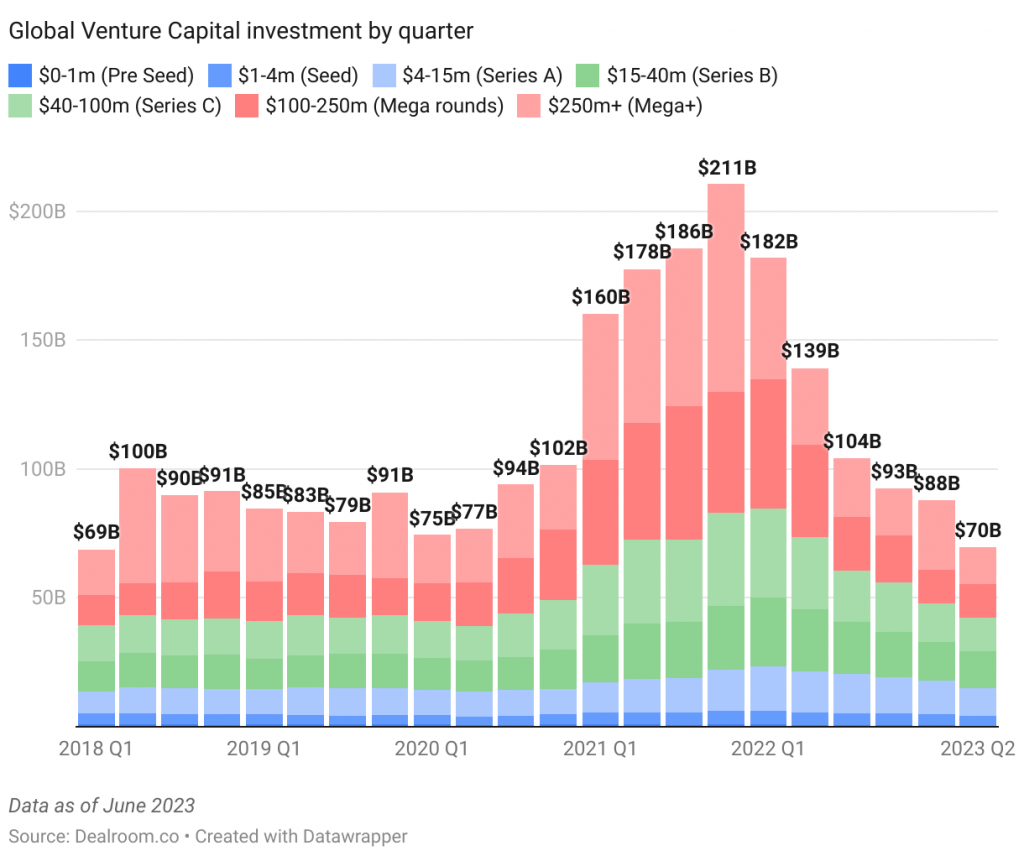

According to Dealroom, VC investments have stabilised around $70-90bn/quarter. This is 50-60% lower than during the pandemic, but in line with the pre-pandemic period.

There is clearly still money being deployed.

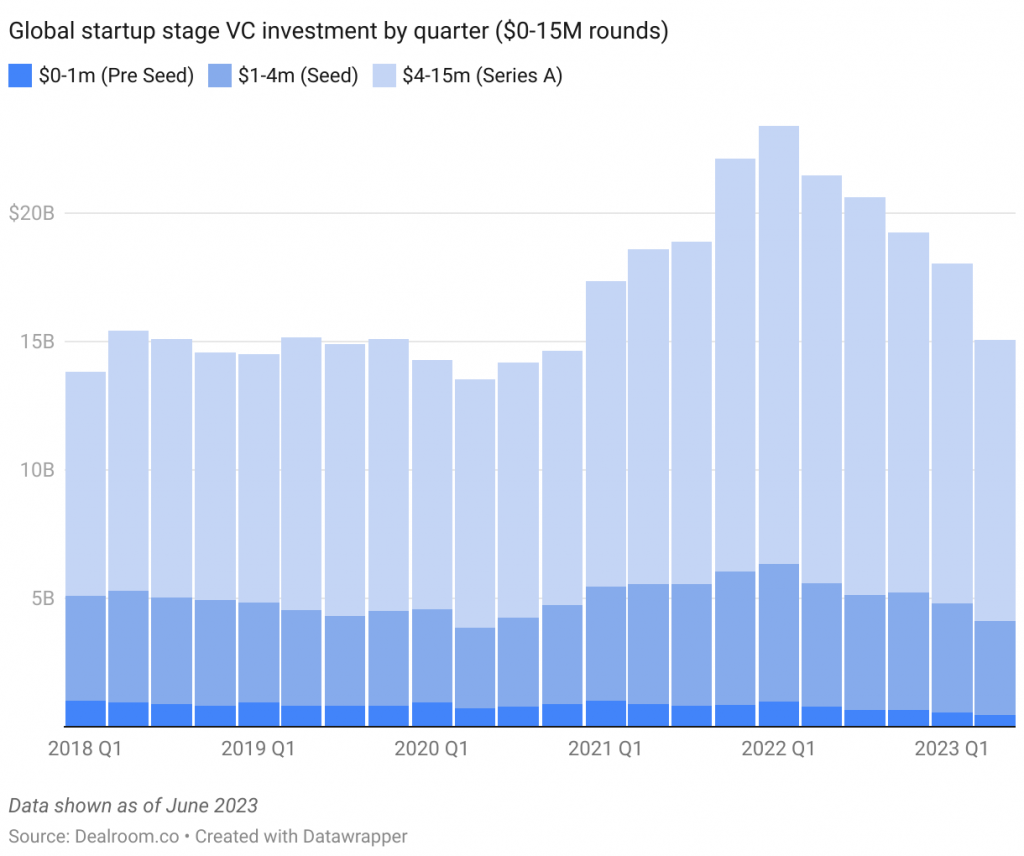

Most of the contraction has been at the later stages. Pre-seed and seed stage investments are declining modestly, but still around $5-6bn/quarter.

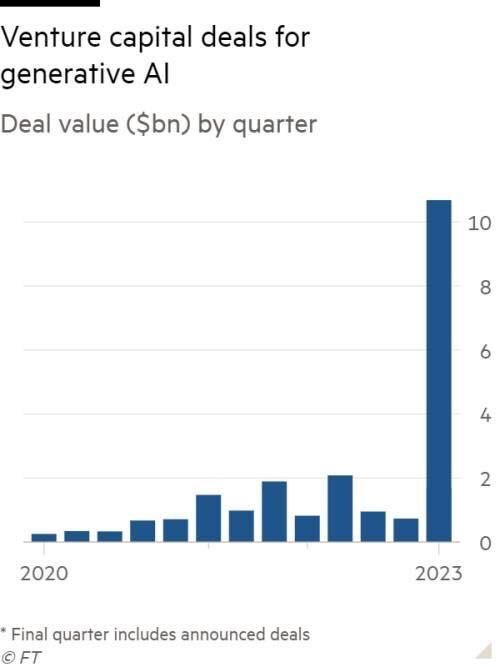

And the type of investments are shifting. We are continuing to see a shift towards SaaS, and generative AI is the hottest area currently.

While some early stage startup have been struggling to raise, AI companies are flying. More than $10bn was invested in generative AI companies in Q1 alone.

As an example, take French Mistral AI that raised a €105m seed round (valued at a post money of €240m). The clincher is that company was only a few weeks’ old. There is specualation that this was a French sovereignty play.

And OpenAI (ChatGPT) competitor Anthropic raised a $450m Series C in May, demonstrating the excitement for generative AI.

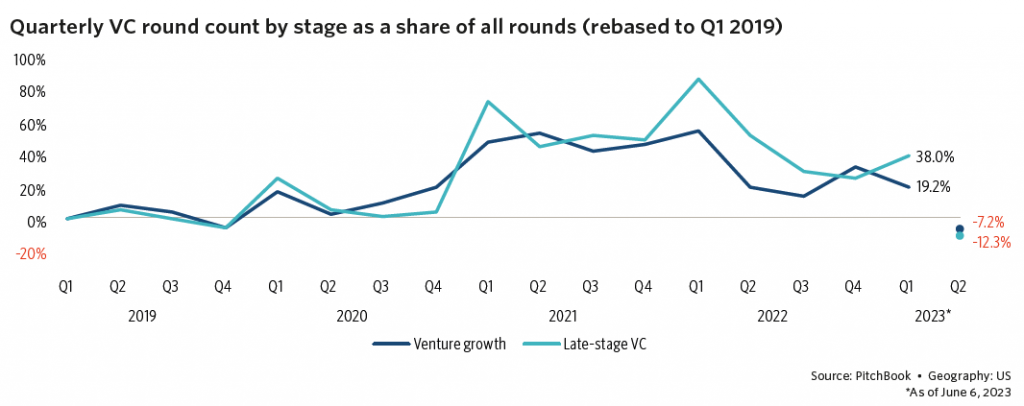

Valuations – Late stage down. Early stage flat/up.

According to Pitchbook, ~35% of growth stage rounds have been down rounds in Q2 (up until the first week of June).

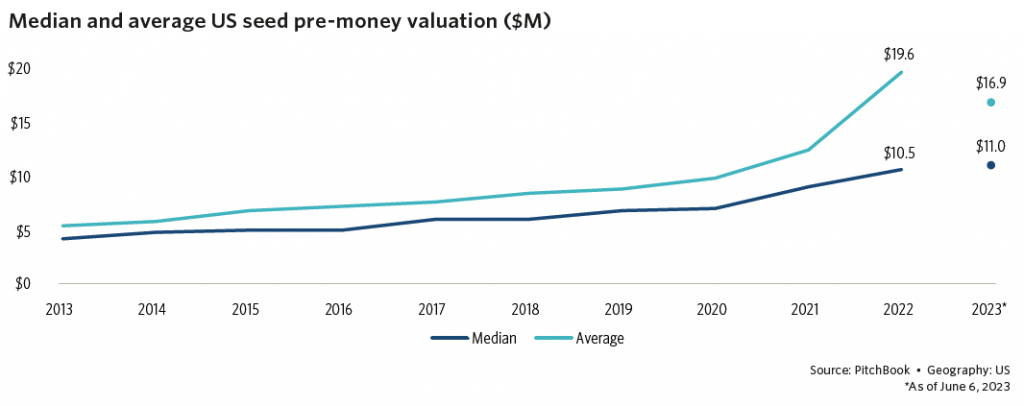

However, the median seed stage pre-money valuation has continue to eke up from $10.5m to $11m (note – these are US figures).

Outside of new investments, secondaries has become the hot area. We have seen 60-70% being knocked off unicorn valuations. Investors are now starting to consider buying secondary shares in former stuperstars that are more attractive investments at lower prices.

The venture ecosystem is surprisingly alive and well

The venture ecosystem certainly took a hit in 2022, but it’s by no means knocked out. Activity is similar to pre-pandemic levels and deals are being done. AI continues to provide disruptive potential, and we see lots of attractive opportunities in the pipeline. More on that below.

SuperSeed Updates

Continued portfolio progress

Despite macro-headwinds, our portfolio revenue continued to grow at a good clip in Q2. Final numbers not yet available, but the forecast says that there is solid progress across the board with some impressive blue-chip customer logos being added in both Europe and the US.

Although the portfolio is still young, we have seen increasing M&A appetite for several of our companies. It is possible that this could lead to early distributions in Q3. We will keep LPs posted.

New investments

In Q2 we also made two exciting new investments in the AI/SaaS space in Q2 (to be announced in the coming weeks), and continue to see strong dealflow.

We have our inagural SuperSaaS one day accelerator for pre-seed companies come up in early June, and we wil be joined by 30 great pre-seed B2B Startups on the day. There are some exciting companies in the cohort – it’s very promising.

In closing

When Dan and I launched SuperSeed in 2018, our focused was ML/AI enabled SaaS. It still is. We expect AI powered software to continue to transform how business is done for the remainder of the decade. It’s a good time to be investing in B2B SaaS companies.