2022 was the year when the laws of physics reasserted themselves in venture capital.

When the music stopped, upside/down business models were brutally exposed. For a while, folks had been launching (and funding) businesses with non-sensical unit economics. Put simply, the idea was to sell $300 suits for $200, and hope to make it up on volume.

In many ways, this was fuelled by a glut of venture capital.

But in 2022, this all came to an abrupt end.

Supply & Demand

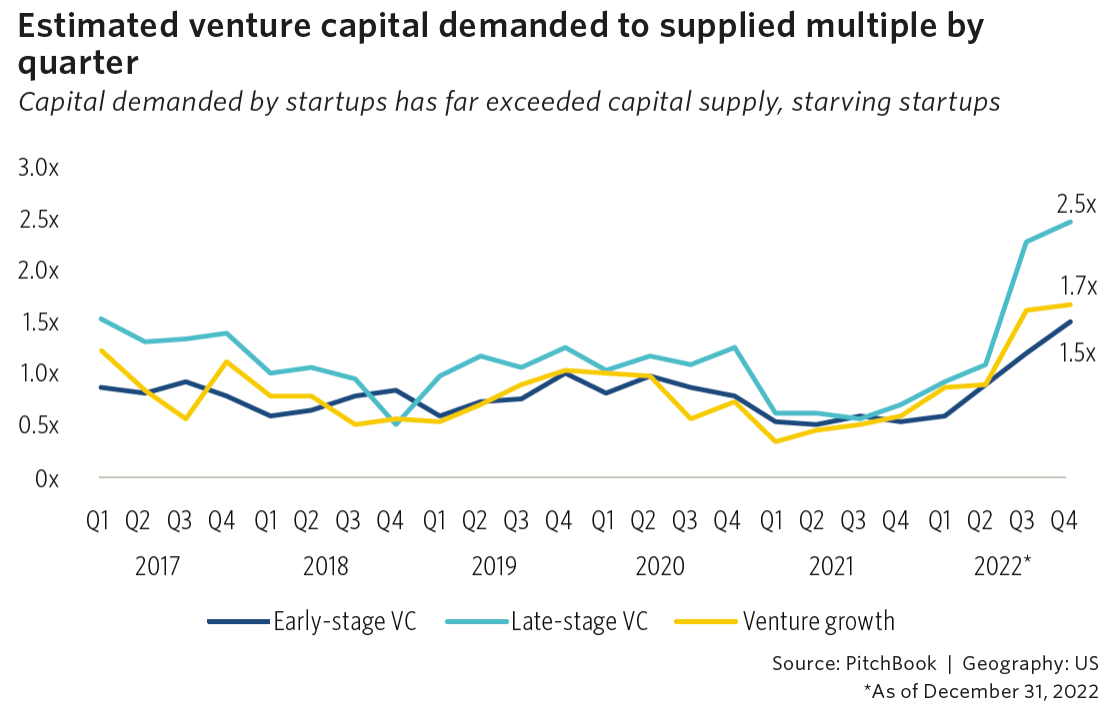

New Pitchbook estimates are in for the supply and demand of VC funding. Pitchbook estimates that Q4 demand in the US outpaced supply by $42.8 billion.

According to Pitchbook, this phenomenon didn’t just apply to late-stage startups. The Pitchbook team estimates that demand at the earlier stage was at least 1.5x supply (and I think that is conservative).

Three Takeaways

- Although there is plenty of “dry powder” in VC funds, a lot of FOMO has come out of the system. Investors are more content to take their time rather than rushing to do deals.

- A lot of companies saddled themselves with far too high cost structures. Many have taken action, but some still “have it all to do”. And some business models are just no longer fundable.

- Many companies were able to put off a raise last year by using convertible notes or stretching runway. But 2023 is going to be a year of reckoning.

Expect continued turbulence in startup land.