This is not investment advice. Always consult your independent financial adviser before making investment decisions.

Chat GPT was released on the 30th of November 2022. We (and many others) thought this was a pretty big deal.

And Presto, 15 months later, NVIDIA hits a $2trn market cap (up 367% since the ChatGPT launch). Obviously, something is going on.

But is this a rerun of the dotcom boom, or are we in the early stages of a different script?

First, the scary parallels.

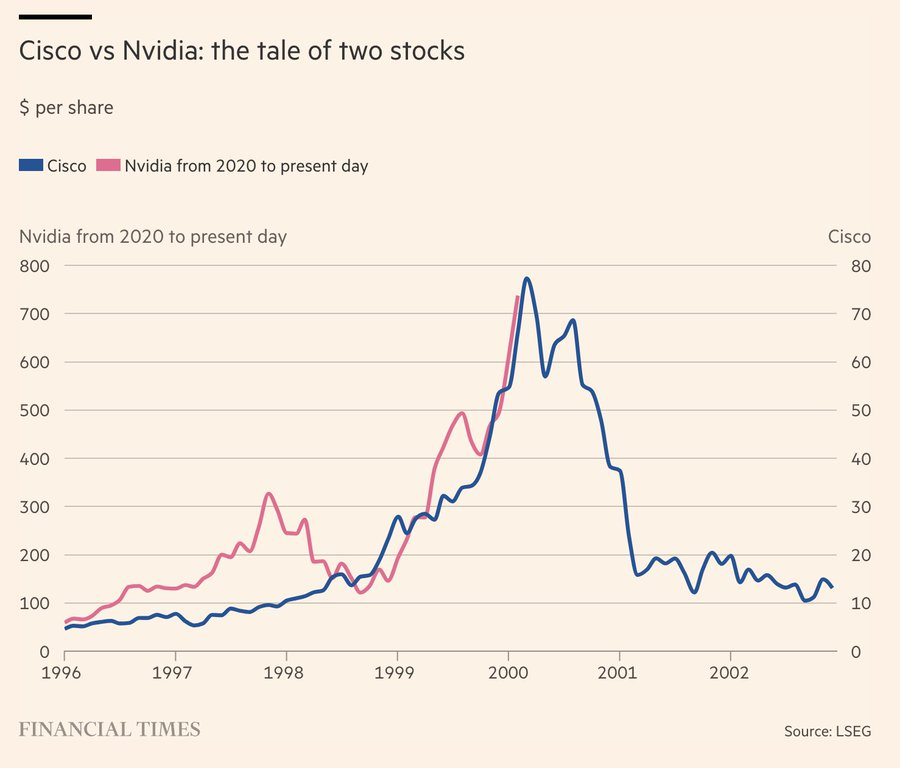

Is NVIDIA the new Cisco?

In the late 90s, the World Wide Web was making the internet useful for consumers, and the tech world was on fire. Lots of dreams for lots of big things, and lots of ways to burn venture dollars (remember pets.com and Webvan?).

But some amazing things also came out of this period – Amazon and Google, to name a couple. And whatever people were building, we all needed more infrastructure. More bandwidth. And more hardware to power our networks. And atop the networking throne was CISCO – the golden child of the Internet’s picks and shovels era.

Today, the Internet is yesterday’s news, and AI is all the rage. We are seeing a plethora of new startups pursue this opportunity. Most won’t succeed in building enduring companies, but there will be great businesses coming out of this. And whether companies are destined for glory or failure, many of them rely on the same thing: the best processors to train and develop their AI models.

And so today’s CISCO is NVIDIA – a company perfectly positioned to be the “picks and shovels” company of the AI revolution.

To hammer home the parallel, the kind folks at the FT recently created this chart that maps CISCO’s ascent in the 1990s to NVIDIAs growth over the past four years. Yes, it has been formatted for maximum scariness. But the comparison is fair.

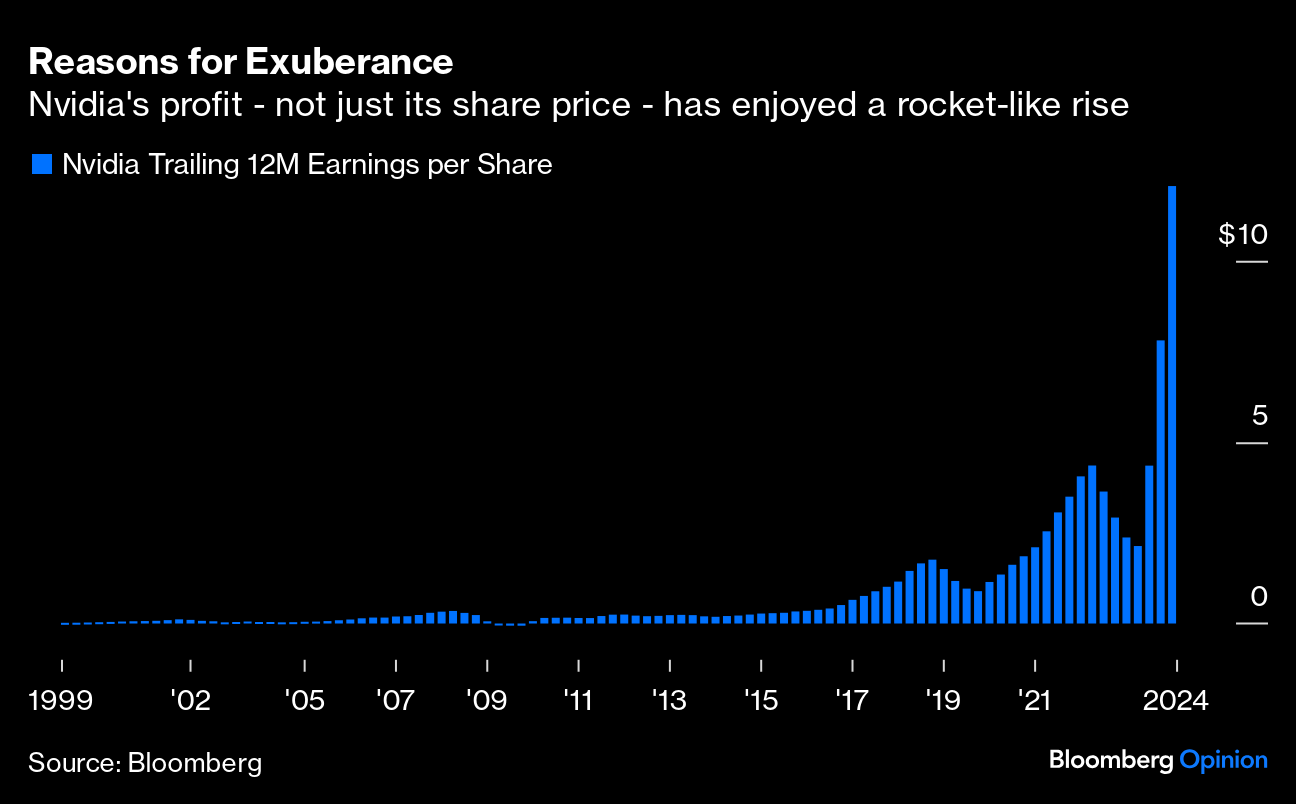

NVIDIA has a strong lead in making chips that can do vector maths (the kind of maths needed to train deep learning and generative AI models). This gives the company incredible pricing power, and profits have been skyrocketing, with the company providing a rosy outlook for the future.

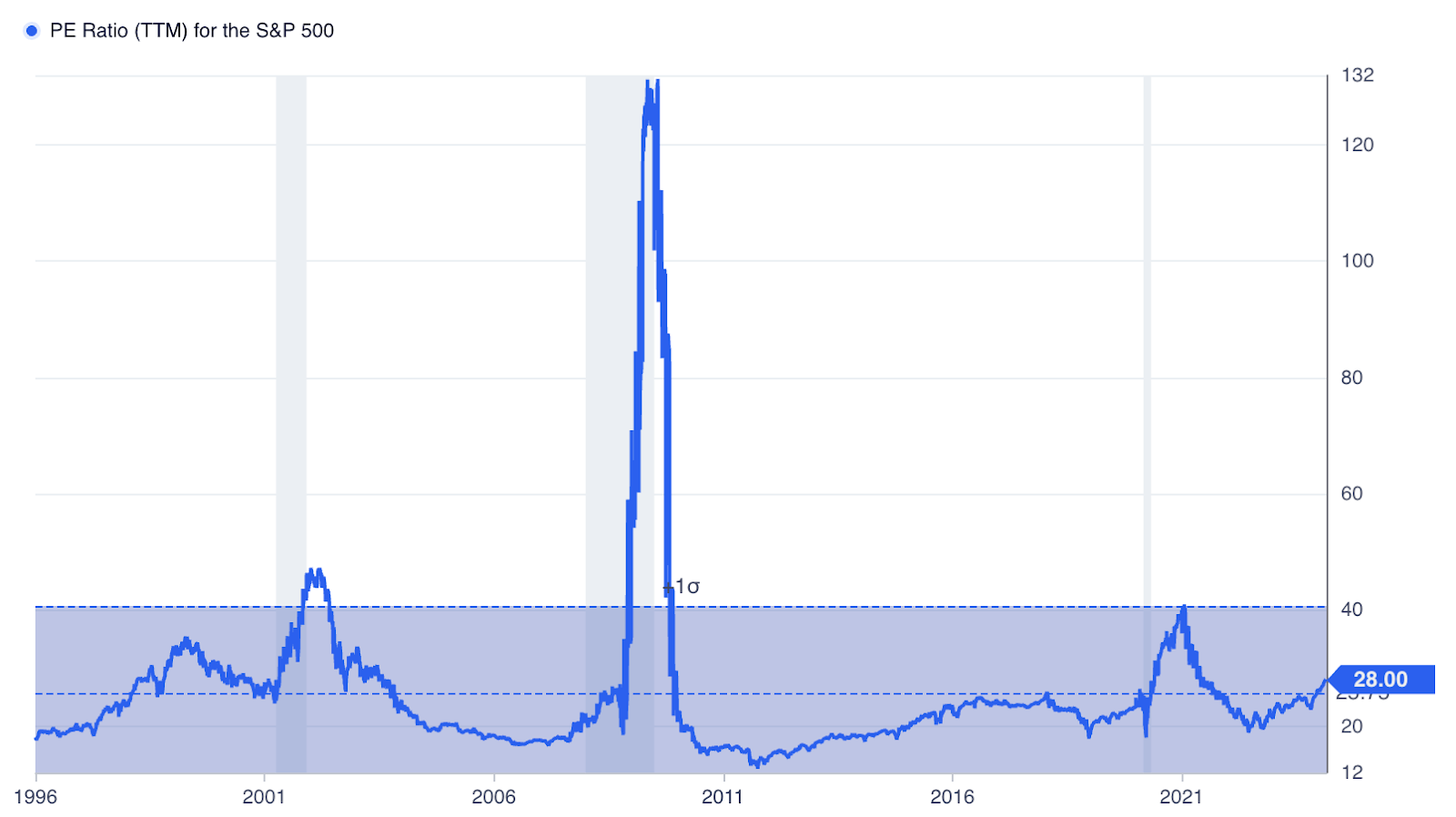

Given the rapid growth in revenue and profit, and given the positive outlook, the buoyant share price seems justified. But at 66x earnings, profit will have to keep growing for some time to justify even the current valuation, leaving alone any upside.

So the question beckons: are we on the precipice of a “dot.ai bubble”, or is there more upside from here?

Let’s look at some more scary data

Have we been here before?

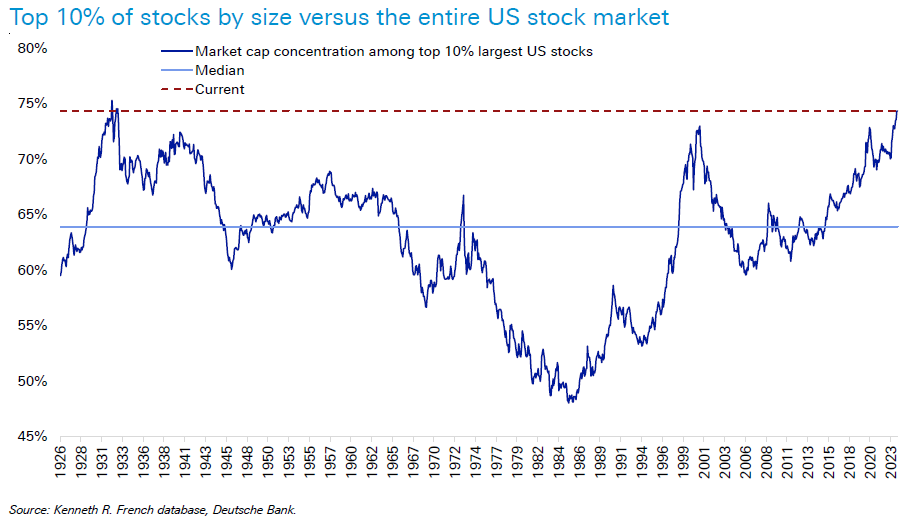

The top 10% of US stocks are currently 75% of the US stock market. The last time that happened was in 2000 1929. And we know what came next.

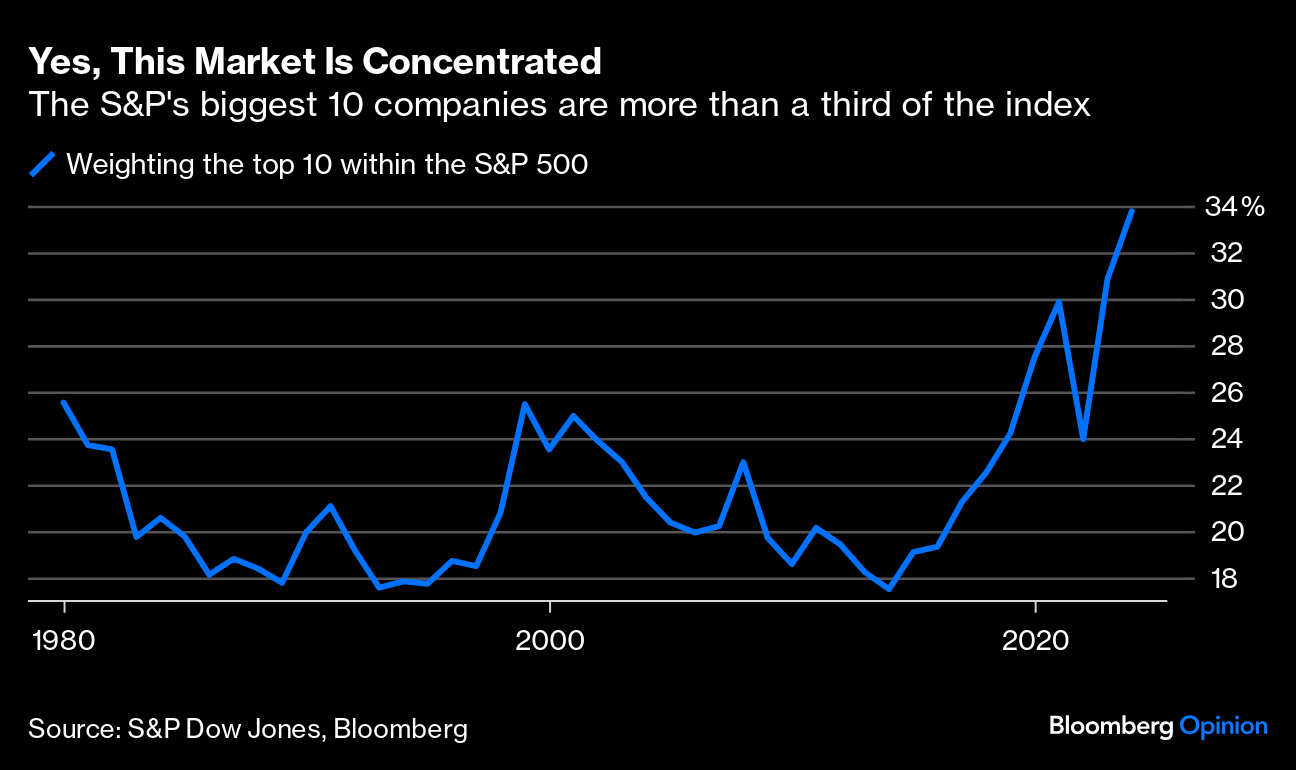

This concentration in the top stocks is driven by the Magnificient Seven. For good measure, let’s add Berkshire Hathaway, Eli Lilly and Broadcom to the mix, and we can see that the top 10 US stocks now account for more than 1/3 of the value of the full market.

There are more ways to show how concentrated and unusual the situation is, but let’s leave it here for now.

So, is it a bubble?

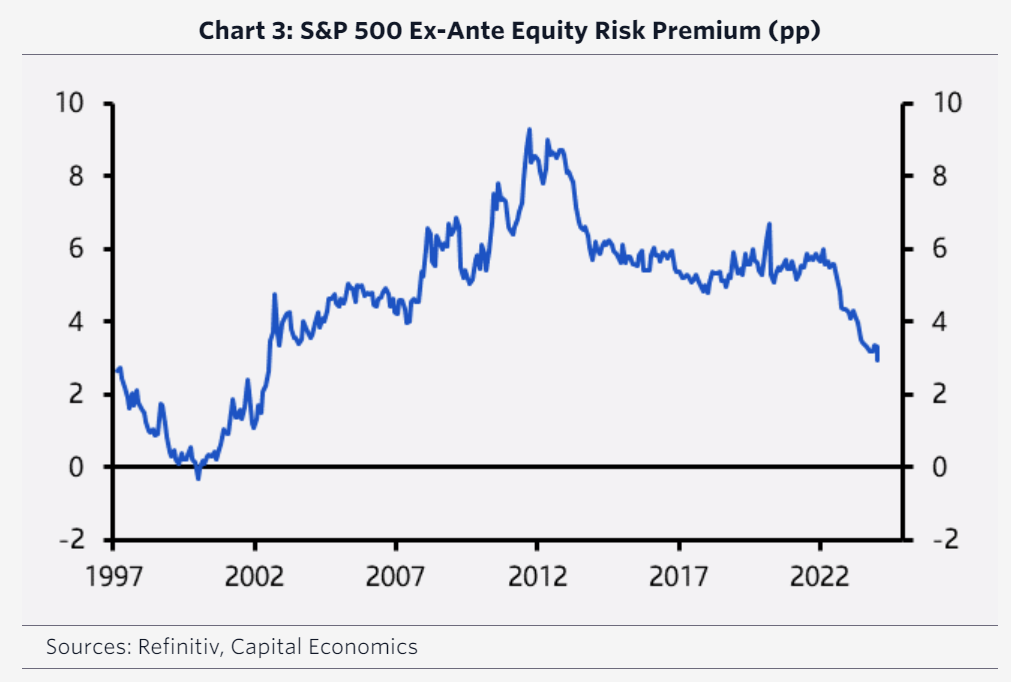

When we measure the stock market using PE ratios and the equity risk premium (i.e. the yield premium you get paid to hold stocks over risk-free bonds), the market looks expensive, but nowhere near as expensive as in 2000 before the dotcom crash (or in the Great Financial Crash, where profits imploded).

If not 2000 all over again, then what?

As I wrote two months ago, stocks look expensive relative to historical metrics. But as long as the top companies keep growing earnings, and as long as there isn’t a major geopolitical event, I don’t expect an implosion in stocks.

At the same time, I am struggling to see NVIDIA go to $7trn (as some people have suggested), but I can easily see the S&P500 go higher from here – at least in the shorter term.

Because althought companies are expensive, there is a major difference now compared to 2000. The best public tech companies are a lot more profitable. And even private companies like OpenAI have grown revenue at an impressive rate, going from basically zero to a $2bn annual run-rate in 13 months (OpenAI hit the $2bn annual run-rate market in December).

While a lot of the investments during the internet boom were well ahead of their time, many of the companies that are being built now have real revenue, strong growth and a path to real profit.

So, where are the private market opportunities?

Firstly, it’s important to distinguish AI as a buzzword vs. AI as “next-generation software”. (Generative) AI feels like magic, but – in my view – it’s really just the next way to create software. And just like mainframes made way for distributed computers that in turn made way for the cloud, so are we now transitioning from a world where software is deterministic to a world where it is probabilistic. It’s a big change with profound implications, but it won’t remove the fundamental value of software. If anything, it just makes software even more valuable, because probabilistic behaviour means that software can do things in ways previously only humans could. For me, the takeaway is: when thinking about AI, think about next-generation software, not magic.

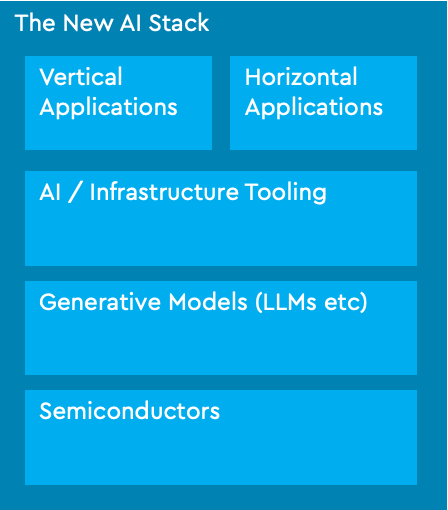

Many investors divide the opportunities into five categories. There are the two layers which have received the most press to date:

- A semiconductor layer populated by incumbents like NVIDIA and new players like Groq.

- A generative model layer with firms like OpenAI, Anthropic, Mistral (and, of course, Google),

On top of these sit three other layers which have received much less press, but where we see incredible innovation right now:

- There is a new class of companies that are creating tools to manage AI models and model infrastructure (e.g. making the AI models more transparent, secure, efficient etc),

- Application companies making vertical applications (industry-specific – e.g. manufacturing or pharma), and

- Application companies making horizontal applications (e.g. sales tools, marketing tools, etc).

Over the past two years, 50% of our investments have been in vertical AI applications. 25% in horizontal AI applications, 15% in AI Infrastructure Tooling, and 10% sit outside mainstream AI use cases (although all do use some level of machine learning).

We see incredible opportunity in those areas going forward, as they are places where smart founding teams can build capital-efficient software companies powered by the new underlying AI capabilities.

Does generative AI spell the end of the software industry?

Software development was one of the first areas to be impacted by generative AI. Armed with ChatGPT or Github CoPilot, developers are now at least 2x as efficient as they were before. It’s become much easier to create, optimise and debug code. This makes it easier to build software. It potentially also makes it easier for new competitors to emerge or for customers to make their own software, as applications can be rebuilt with less effort.

Some observers have speculated that this is the end of the SaaS industry. That AI makes it so easy to create new software that margins will be competed away or replaced by new in-house apps.

There is some sense to these arguments. But in many ways, this was also what people said about the software industry when open source emerged.

The modern software industry is incredibly reliant on open-source software. And open source did displace some companies (e.g. how the once mighty Sun Solaris made way for Linux). But as some companies got displaced by open source, the wider software industry continued to thrive. Open Source was an enabler for the software industry.

Here are two reasons why I predict that AI will also be an accelerator for the SaaS industry:

- Yes – Generative AI makes it easier and cheaper for new entrants to create software clones. But it also makes it easier for independent software firms to innovate rapidly. And independents are nimble and focused. While Generative AI gives many new weapons to rebellious startups, it will also confer big advantages on startups. I predict that this will lead to a continued thriving software ecosystem.

- Generative AI also makes it easier for in-house development teams to build their own platforms. And while this gives them an advantage when negotiating pricing, it will not replace external software vendors for the same reasons corporates buy software today. Most businesses are much better off getting best-of-breed from specialist vendors rather than crafting and maintaining their own systems. Not only because it is expensive and inefficient for everyone to build and maintain essentially the same thing, but also because specialist vendors are better at innovating and, therefore, providing a better platform and user experience.

We’ve heard the same story about infrastructure and compute many times. It’s cheaper to buy your own servers than to rent them from AWS. Yet 87% of Fortune500 companies today use at least one public cloud.

One of Jeff Bezos’ business maxims is to only do the things that “make your beer taste better”. As in, focus on the things that make a tangible difference to your customers. Running your own data centres and writing your own backoffice software is unlikely to do that for most companies. And so, our investment strategy remains focused on next-generation, AI-powered B2B SaaS companies. In our assessment, AI will only serve to make this business model even more attractive.