We are now well into the summer period, and this month we look at liquidity in venture capital and the threat of a return of inflation.

Liquidity in venture capital

Last month we examined how H1 of 2021 has been a record year for the amount invested in venture capital. A significant portion of this investment was in mega growth rounds (+$250m) that have set records. From our perspective, it is positive to see so much capital allocated to grow tech companies at the later stages. One of the critical drivers for this growth is the success of the IPO market. Although there have been initial disappointments like the Deliveroo IPO in April, that stock has since recovered (up over 17% since April 1st). And many others (like Darktrace) have done phenomenally well post IPO.

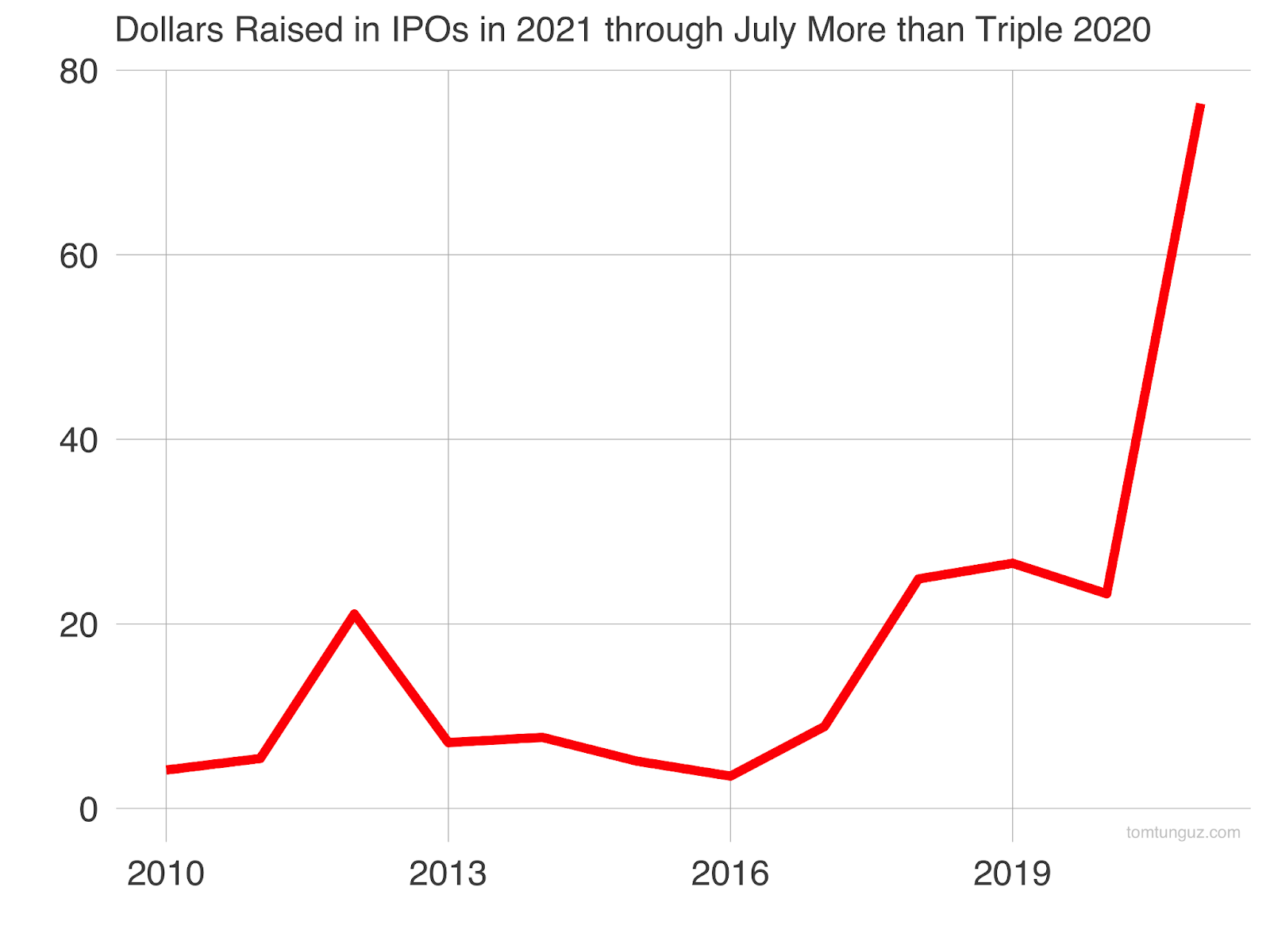

Half a decade ago, there was a dearth of IPOs, which meant that it took longer for VC investors to turn profits into cash. This situation has now been turned entirely on its head. In the first half of 2021, the amount of dollars raised through IPOs in the US was more than triple all of 2020. Some of this is driven by SPACs, and there are reasonable criticisms of the recent SPAC surge. However, a large part of the IPO proceeds is ultimately finding its way back into the venture eco-system – first as distributions to investors and then as investments into the next wave of early startups.

In 2015, VC backed companies accounted for 44% of the R&D spend of all US public companies – a number that’s likely only gone up since then. Therefore, we see the IPO liquidity flowing through the startup ecosystem as positive – both for investors and the wider economy.

Is inflation coming back?

For the past 30 years, we have lived in a blissful world of declining inflation, with OECD averages down from ~10% p.a. in the 80s to ~2% in the noughties (FT Paywall)

However, this year, the spectre of inflation has been rearing its head again, with the US Core Consumer Price Index (CPI) up 4.5% year-over-year in June. This is the largest increase in the CPI since November 1991, and it has rightly gotten many observers concerned that inflation is on the march.

Why should we care?

Besides the obvious (rising prices and erosion of purchasing power), increasing inflation might force central bankers to raise interest rates. This could have a double whammy effect. It could:

- put a damper on economic activity, which would slow earnings growth, and

- mean that a higher rate of interest should be used when discounting expected future cash flows (still the primary way to value public companies). In other words – not a promising scenario.

But is there a likelihood that the inflation fears are overblown?

The Nobel Prize-winning economist Paul Krugman recently analysed this issue, and he suggested two major reasons for why inflation might not be as threatening as some think:

- A large part of the increase in CPI has been driven by the increasing price of cars, which, in turn, was caused by shortages in the supply chain – primarily from semiconductors (yes – cars are really driving computers nowadays – Marc Andressen was not wrong). TSMC, which is one of the largest suppliers of chips to the automotive industry, said in mid-July that they would ramp production by 60% this year. As these types of supply chain bottlenecks get cleared up, that will help take the pressure off inflation.

- Although consumption was down in 2020 (and with it – GDP), most of the slump was in perishable goods and services (vacations, restaurant visits, haircuts). In contrast, investment in durable goods like TV’s and refrigerators held up just fine. So although savings rates were up and there theoretically is a lot of money ready to be spent (which could cause inflation), it is unlikely that we will all suddenly go have a year’s worth of haircuts or restaurant meals all at once. There is just a limit to how many of those perishable goods we can consume – even if we have been deprived for too long.

So what does this mean for UK interest rates? According to the Bank of England, it doesn’t look like rate increases are imminent (FT: paywall). But it’s certainly worth continuing to keep an eye on inflation as we enter the next phase of the post-covid recovery.