The Bill Has Arrived

Europe reluctantly accepted 15% tariffs from the United States last month. There were negotiations, attempts to find alternatives, diplomatic manoeuvring – but ultimately, something close to surrender. The EU acknowledged it lacked the levers to fight back effectively. The reason, whispered in Brussels but never stated plainly: we spend 2% of GDP on defence while relying on American protection that costs them 3.5%. The arithmetic finally came due.

This is Trump being transactional, yes – but it’s also structural reality. Both things are true. The US calculation has shifted: providing global security guarantees no longer automatically translates to economic dominance when others might build better products. So now the security umbrella comes with an explicit price tag. The EU-US trade deal represents something new in European history: sovereignty as a subscription service, with the vendor adjusting rates based on market conditions.

The surprise isn’t that America presented the bill. The surprise is that we’re still surprised. Every dependency creates leverage. Every leverage point eventually gets monetised. The comfortable assumption that security and economics operated in separate spheres – that assumption just ended.

How We Got Here

The dependencies seemed like rational choices at the time, but ultimately turned out to be mistakes – traps that snapped shut when the world changed.

Defence: The Peace Dividend Trap

Outsourcing defence to America freed up 2% of GDP for social programs and infrastructure. It worked from 1945 to 2024. The peace dividend funded the European social model we’re justly proud of. Then the bill arrived in the form of tariffs.

Energy: The Cheap Gas Illusion

The energy dependency was always a vulnerability. Europe has paid higher energy costs than the US and China for decades. The reliance on Russian gas – particularly acute in Germany since reunification – was a mistake in 2005 precisely because of where it led us today. When Russia invaded Ukraine, we discovered the price of that dependency. France’s nuclear independence and Norway’s energy surplus couldn’t compensate for Germany’s industrial heart being exposed.

Manufacturing: The Clean Cities Trade-off

Outsourcing manufacturing to China gave us cleaner cities and cheaper goods. We exported our emissions and imported our products, meeting climate targets while maintaining living standards. It seemed rational – until supply chains became weapons and industrial capacity determined technological sovereignty.

The Comfortable Middle Path

Each decision is optimised for the immediate benefit while creating a future vulnerability. We confused a favourable environment with a permanent condition. We chose the comfortable middle path – maintaining the appearance of strategic autonomy while deepening actual dependencies. It worked as long as no one called the bluff.

Dependency by dependency, we’ve traded autonomy for comfort. Now the bills are arriving, and we’re discovering that sovereignty isn’t free – it just seemed that way when nobody was charging.

The Wake-Up Call

Three things changed in 2025 that make the sovereignty question unavoidable.

The Bills Became Explicit

First, the bills became explicit. Trump’s tariffs aren’t abstract economic theory – they impact our exporters directly by making them less competitive. When Ørsted’s wind contracts were cancelled over Greenland access, the message was clear: even close allies face economic consequences when strategic interests diverge.

The Alternatives Became Visible

Second, the alternatives became visible. China’s industrial policy – mocked for years as wasteful – delivered results. They funded 500 EV companies, watched 485 fail, and the 15 survivors now dominate global markets. While we debated market efficiency, they built market dominance. The lesson isn’t that we should copy China, but that strategic sectors require strategic thinking.

The Technology Shifted

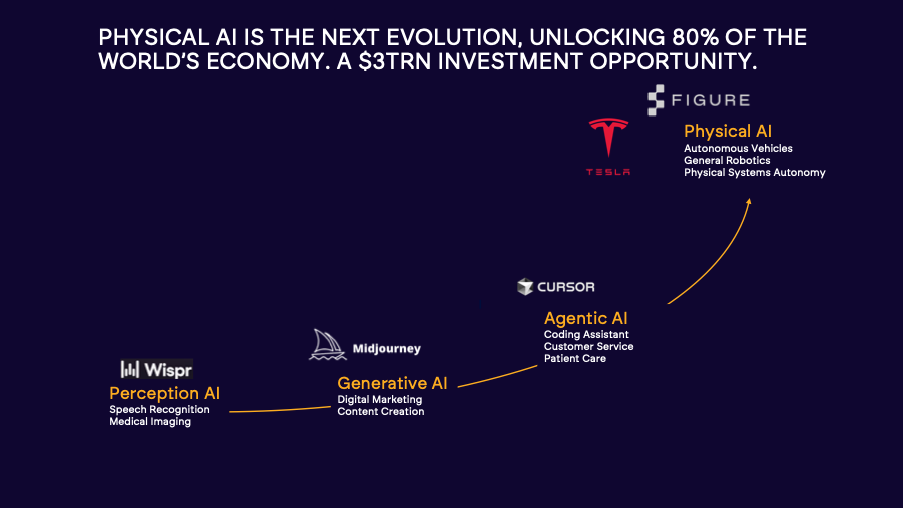

Third, and most important: the technology shifted. We’re entering the age of Physical AI, and for the first time in two decades, Europe has structural advantages.

Consider the evolution: Perception AI in the 2010s meant computer vision and voice recognition – the US dominated through data advantages. Generative AI in the 2020s meant LLMs and image generation – the US won through compute and capital. Agentic AI today means workflow automation – and European companies like n8n and Loveable are competing effectively.

But Physical AI – robotics, manufacturing automation, energy systems – is different. We have the factories that need automating. We have the engineering heritage (ASML makes machines precise to the atomic level). We have the industrial customers who understand that making things still matters. Europe produces 19% of global manufacturing output versus America’s 17%. That’s not a legacy burden – it’s a launching pad.

The irony is perfect: just as we seemed resigned to permanent technological dependence, the technology itself shifted toward our strengths.

The Path Forward

The comfortable illusions must end. Industrial policy works when executed well – ask TSMC or BYD. Free markets alone won’t restore sovereignty when others are playing by different rules.

Building European technological sovereignty requires three elements: talent to create, customers to buy, and capital to scale. We have the first – Europe produces more STEM PhDs than America, more software developers in absolute numbers. The second is fixable through procurement reform. But the third – capital – is the bottleneck that strangles everything else.

The Capital Crisis

A critical part of America’s success is the depth of its capital markets. More capital flows to large listed companies, mid-stage growth companies, and early-stage startups. Every rung of the ladder matters. US venture capital investment runs at $585 per capita versus Europe’s $104 – a 5.6x difference. This isn’t random; it’s structural.

The root cause lies in how we deploy savings. American and Canadian pension funds define prudence as maximising long-term returns – the correct lens for retirement savings with decades-long horizons. European funds define prudence as minimising short-term volatility – utterly wrong for long-term savings. The result: European pension funds allocate much less than US counterparts to equities and other productive assets.

Worse, too much of the European equity investment goes abroad. UK pension funds now allocate just 4.4% to UK equities – their lowest level ever. We’re not just conservative; we’re conservative AND we export our risk capital.

Nobody suggests forcing European savers into European equities – least of all venture capital. But consider this: The UK alone spends £52 billion annually subsidising pension savings through tax relief. These subsidies apply whether investments go to Nasdaq, London, or Frankfurt. Why should British and other European taxpayers subsidise the provision of capital to US megacaps?

The fix requires two changes:

1. Make pension tax relief conditional – full benefits only for European productive assets

2. Redefine fiduciary duty from volatility minimisation to long-term value creation

Fix these, and we unlock more capital flows across the entire ladder – from venture to growth to public markets. Long-term returns to savers increase. GDP growth accelerates. Innovation thrives.

Strategic Sectors

Focus is essential. Ten sectors will determine technological sovereignty: semiconductors, energy storage, critical materials, AI, biotech, defence and aerospace, quantum computing, telecommunications, robotics, and autonomous vehicles. No single European country can lead them all. So we must work together with our closest partners. UK-EU collaboration isn’t nice to have, it’s a necessity.

The Choice

The sovereignty invoice grows monthly. Every delayed decision compounds the cost. But we have everything needed to pay it down.

We have more STEM PhDs per capita than America. Our industrial base remains formidable – 19% of global manufacturing. When European entrepreneurs and engineers get the resources they need, they build world-leading companies. ASML dominates semiconductor equipment globally. Airbus has surpassed Boeing in commercial aviation. Siemens leads industrial automation. Ericsson and Nokia anchor global 5G infrastructure. The lesson isn’t to pick champions – it’s to create conditions where thousands can compete and the best naturally emerge.

For investors, the opportunity is historic. European B2B startups create more than 2x as much revenue per invested € as their US peers – not through miracles but through discipline. And according to Cambridge Associates, European venture capital has already delivered better returns than our US counterparts over the past 10 and 15-year horizons. But there is so much more we can do. And the new geostrategic reality suggests that we better get started on that work asap.

The sovereignty invoice isn’t about choosing autarky over openness. It’s about building strength in what matters while trading freely in what doesn’t. Europe doesn’t need to make every widget or write every app. But when our energy, defence, and digital futures depend on foreign goodwill, we’re not sovereign – we’re subscribers.

The bill is due. We can pay it by building strategic autonomy in critical sectors, or we can continue managing decline. What we can’t do is pretend the choice doesn’t exist.

The comfortable middle path just closed.